Never trust anyone – not your spouse, friends, neighbours, colleagues, bosses, politicians, religious leaders, gods, news outlets, or even the weatherman or stock market forecasts. And certainly not yourself. Always verify information across multiple languages, sources, perspectives, timeframes, and under different political and economic regimes. Remember – in the world of money, you are your only true ally, and “there are no facts, only interpretations” (Friedrich Nietzsche). Always ask: Who stands to profit from the advice, analysis, or opinion you’ve just been given?

And remember: “Life is a tricky thing: just when you have all the cards in your hands, it suddenly starts playing chess.”

General section:

"Fake it till you make it" - How to sound like a trading guru:

Don't catch the falling knife:

Probably the best advice no one ever takes on board: Buy the S&P 500 Index and forget all about it

The long run in words

“Those classes of investments considered ‘best’ change from period to period. The pathetic fallacy is what are thought to be the best are in truth only the most popular—

the most active, the most talked of, the most boosted, and consequently, the highest in price at that time.” Fred Schwed Jr.

“Markets stop panicking when central banks start panicking.” BofA Strategist

“When all the experts and forecasts agree – something else is going to happen.” Bob Farrell

“If there are two rules in investing they are that magnificent portfolios attract inflows, and inflows ultimately destroy magnificent portfolios.” Eric Peters

“Buy on the cannons, sell on the trumpets.” Baron Rothschild

“We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.” Warren Buffett

“Successful investing is anticipating the anticipations of others.” John Maynard Keynes

“The four most dangerous words in investing are ‘This time it’s different.’” John Templeton

“There are two types of forecasters: those that don’t know, and those that don’t know they don’t know.” John Kenneth Galbriath

"Little else is requisite to carry a state to the highest degree of opulence from the lowest barbarism but peace, easy taxes, tolerable administration of justice." Adam Smith

“Wall Street’s favorite short is always ‘denial’ and Wall Street’s favorite long is ‘panic’.” BofA Strategist

“There are only three ways to meet the unpaid bills of a nation. The first is taxation. The second is repudiation. The third is inflation.” Herbert Hoover

“Inflation is like toothpaste. Once it's out, you can hardly get it back in again.” Karl Otto Pohl

“Nothing is so permanent as a temporary government program.” Milton Friedman

“There are no new eras—excesses are never permanent.” Bob Farrell

“The average long-term experience in investing is never surprising, but the short-term experience is always surprising.” Charles Ellis

“Buy humiliation, sell hubris.” BofA Strategist

“Markets can remain irrational longer than you can remain solvent.” John Maynard Keynes

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it." Albert Einstein

“In economics, things take longer to happen than you think they will, and then happen faster than you thought they could.” Rudiger Dornbusch

“Never in the field of monetary policy was so much gained by so few at the expense of so many.” BofA Strategist on 2010s

“Speculation is an effort to turn a little money into a lot. Investment is an effort to prevent a lot of money from becoming a little.” Fred Schwed Jr.

“If all the economists were laid end to end, they’d never reach a conclusion.” George Bernard Shaw

“Past performance is not necessarily a guide to future performance.” SEC requirement

“The long run is a misleading guide to current affairs. In the long run we are all dead.” John Maynard Keynes

“I can show, really precisely, that there are two warranted prices for a share. The one I prefer is based on such fundamentals as earnings and growth rates, but the bubble is rational in a certain sense. The expectation of growth produces the growth, which confirms the expectation; people will buy it because it went up. But once you are convinced that it is not growing anymore, nobody wants to hold a stock because it is overvalued. Everybody wants to get out and it collapses, beyond the fundamentals.” - Franco Modigliani, Nobel Laureate, March 30, 2000, New York Times

This man wrote 10 lines studied by even the smartest investors. Yet, his 10 rules are more useful than 10,000 hours of CNBC.

Here’s Bob Farrell’s “common sense” guide to uncertain markets:

Markets return to the mean Extreme prices never last. For eg: The S&P 500 fell 34% in March 2020, then fully recovered by August.

Excess in one direction leads to the opposite Bubbles create busts. For eg: The dot-com bubble drove tech sky high… then crashed the Nasdaq by ~78%.

There are no new eras “This time is different” is costly. For eg: Pre-profit stocks were unstoppable in 2021. In 2022, they weren’t.

Fast moves don’t end gently Parabolic rises collapse hard. For eg: Bitcoin rose 7x in a year, then dropped 75%.

The public buys tops, sells bottoms Crowds chase comfort, not value. For eg: Retail piled in near highs in 2021, then fled in 2022.

Fear and greed beat resolve Plans are easy. Sticking to them isn’t. For eg: Many sold at the bottom in March 2020 and missed the recovery.

Broad markets = strength When only a handful of stocks lead, it’s a warning. For eg: In 2023, 7 tech giants drove most of the S&P 500.

Bear markets have 3 stages Sharp fall → reflex rebound → long, grinding downtrend. For eg: The 2008 crash dragged on for months, not weeks.

When everyone agrees… expect the opposite If all are bullish, who’s left to buy? For eg: In Jan 2022, most analysts predicted a strong year. The market sank instead.

Bull markets are fun, bears are painful Everyone looks smart when prices rise. But real fortunes are made in bear markets… if you can survive them.

Farrell’s rules aren’t strategies. They’re reminders:

Markets swing

Emotions lie

History repeats

Ignore these truths, and the market will teach them to you - the hard way.

Growth is the best long-term predictor of a stock market winner

The long run in years

1602: the Dutch East India Company becomes the first company to issue stocks and bonds on the Amsterdam Stock Exchange

1685: Germany establishes the second stock exchange in the world

1790: an $80 million US Government bond offering to refinance Revolutionary War debt becomes the first publicly traded security in the US

1792: the NYSE is established and the Bank of New York becomes the first company listed

1810: Russia is the first “emerging market” country to establish a stock market

1821: Great Britain adopts the gold standard

1862: US stocks record their best year ever, returning 70%

1891: the first US equity bear market (>20% loss) is caused by the “Baring Brothers Crisis”

1918: record high in US inflation rate of 20.4%

1923: hyperinflation in Germany, $1 worth 4,210,500,000,000 German marks

1929: Wall Street Crash signals beginning of Great Depression

1930: US implements Smoot-Hawley Act raising tariffs on more than 20,000 imported goods.

1931: US stocks record their worst year ever, declining 43%

1933: US unemployment peaks at 25%, President Franklin D. Roosevelt launches “New Deal”

1948: hyperinflation in Japan, consumer prices rise 5,300%

1971: “Nixon shock” as US ends convertibility of US dollar to gold, ending Bretton Woods; US dollar becomes a fiat currency

1981: monthly US 10-year Treasury yields hit an all-time high of 15.8%

1982: the best year of total return for long-term Treasuries of 40%

1987: on “Black Monday” October 19th, the Dow falls 23%, the largest daily drop ever

2001: China becomes member of World Trade Organization

2007: 1st iPhone launched

2008: Global Financial Crisis…US financial stocks fall 57%

2009: Fed launches Quantitative Easing

2011: US debt downgraded by Standard & Poor; gold price hits record high of $1900/oz

2014: Fed ends QE program; oil begins brutal bear market ($107/bbl to $26/bbl in Feb’16)

2016: Bank of Japan announces negative interest rate policy; TPP (Trans-Pacific Partnership legislation) not ratified by US Congress

2017: US stock volatility hits 50-year low

2018: S&P500 becomes longest bull market of all-time; US/China trade war begin

2019: US economic expansion became the longest since Civil War; US budget deficit hits $1tn

2020: COVID-19 pandemic begins; US unemployment rises 33mn; equity market crashes $30tn; global GDP crashes $9tn; interest rates drop to 5,000-year lows

2021: COVID-19 monetary & fiscal policy stimulus totals $28tn; Bitcoin hits all-time high at $68,992; Apple 1st company to hit $3tn market cap

2022: Russia-Ukraine War; Fed starts most aggressive rate hiking cycle in 40 years; worst loss (17%) in 10-year Treasury since 1788; S&P 500 crashes from 4.8k to 3.5k

2023: India surpasses China population; 2nd US debt downgrade; US Treasury losses for 3rd consecutive year; ChatGPT ignites AI “baby bubble”.

The long run in numbers

5000 years: on Mar 9th 2020 the US 10-year Treasury yield fell to an intraday low of 0.3%, taking global interest rates to their lowest level in 5000 years

520: central bank rate hikes in the past 24 months (vs. 1351 rate cuts since Lehman bankruptcy in 2008)

$5tn: liquidity drain by global central banks since 2022 (vs $34tn liquidity injection from 2008 to 2022)

31%: Fed balance sheet as % of GDP…was 0% to 3% during WWI, 2% to 11% during WWII, 6% to 15% after GFC, hit high of 37% after COVID

44%: US government spending % GDP…peaked at 24% in WWI, 44% in WWII, 43% after GFC, hit high of 54% after COVID

40%: growth of US economy in past 3 years in nominal GDP terms, fastest expansion since 1975-79

26 million: US jobs created since Apr 2020 (follows 22 million jobs lost Mar-Apr 2020)

2 billion: number of people that experienced inflation of >10% in 2022 (quarter of global population)

$6.9tn: proposed US federal budget for 2024 would make US government 3rd largest economy in the world

$33.6 trillion: US government debt, more than combined GDP of China, Japan, Germany, India, and rising $5.2 billion every day

3: US Treasuries on course for 3rd consecutive years of negative returns, first time in 246-year history of US republic

75%: loss on 100-year Austria government bond since Dec 2020

52%: Americans more concerned than excited about increased use of AI (vs 10% more excited than concerned & 36% who say both)

4.1 million: workdays lost to strikes in the US in Aug 2023, most since 2000

3.6%: Japanese wage growth in 2023, highest in 30 years

21.8%: China youth unemployment at record high in Jun 2023 (series discontinued in Aug 2023)

800 million: decline in China’s current population of 1.4 billion by 2100

$1.5tn: annualized YTD inflow to money market funds in 2023, on course for record year

$4.9 trillion: peak market cap gain of “Magnificent Seven” in 2023, a gain greater than GDP of Germany (tech at all-time high vs. S&P 500)

1926: US bank stocks at lowest level vs. S&P 500 since 1926

1971: US equities at highest level vs Emerging Market equities since 1971

-8.6%: price return of MSCI All Country World Equal-Weighted Index (contains 2,947 stocks) since Jan 1st 2020

9914: average gain in 14 US equity bull markets in past 100 years…177% in 59 months….history says S&P500 hits peak of 9914 in Sep 2027

2043: average time for US stocks to regain new highs in real terms after secular peak…22 years…history say S&P500 hits new highs in real terms in 2043

Market Wizard Linda Reschke’s 12 Technical Trading Rules:

1. Buy the first pullback after a new high. Sell the first rally after a new low.

2. Afternoon strength or weakness should have follow through the next day.

3. The best trading reversals occur in the morning, not the afternoon.

4. The larger the market gaps, the greater the odds of continuation and a trend.

5. The way the market trades around the previous day’s high or low is a good indicator of the market’s technical strength or weakness.

6. The previous day’s high and low are two very important “pivot” points, for this was the definitive point where buyers or sellers came in the day before. Look for the market to either test and reverse off these points, or push through and show signs of continuation.

7. The last hour often tells the truth about how strong a trend truly is. “Smart” money shows their hand in the last hour, continuing to mark positions in their favor. As long as a market is having consecutive strong closes, look for up-trend to continue. The up trend is most likely to end when there is a morning rally first, followed by a weak close.

8. High volume on the close implies continuity the next morning in the direction of the last half-hour. In a strongly trending market, look for resumption of the trend in the last hour.

9. The first hour’s range establishes the framework for the rest of the trading day.

10. A greater percentage of the day’s range occurs in the first hour then was the case in the past, and thus it has become increasingly important to trade aggressively if there are early signs of a strong trend for the day.

11. There are four basic principles of price behavior which have held up over time. Confidence that a type of price action is a true principle is what allows a trader to develop a systematic approach. The following four principles can be modeled and quantified and hold true for all time frames, all markets. The majority of patterns or systems that have a demonstrable edge are based on one of these four enduring principles of price behavior. Charles Dow was one of the first to touch on them in his writings:

Principle 1: A Trend Has a Higher Probability of Continuation than Reversal

Principle 2: Momentum Precedes Price

Principle 3: Trends End in a Climax

Principle 4: The Market Alternates between Range Expansion and Range Contraction!

12. In the world of money, which is a world shaped by human behavior, nobody has the foggiest notion of what will happen in the future. Mark that word — Nobody! Thus the successful trader does not base moves on what supposedly will happen but reacts instead to what does happen.

Peter Lynch’s 25 Golden Rules for Investing

The Big Picture:

S&P 500 Index around military invasions and conflict:

Labor unions metter:

US asset & sector returns by decade, Investor takeaways:

• In decades of deflation (1930s), bonds outperform stocks.

• In decades of reflation (1940s), stocks outperform bonds.

• In decades of high inflation/stagflation (1970s), real returns from stocks and bonds are poor.

• In decades of disinflation (1980s, 1990s), real returns from stocks and bonds are very good.

• In the following decade of disinflation (2000-2009), bonds and commodities significantly outperformed stocks; only the energy, consumer staples and utility sectors recorded positive equity returns.

• In the prior decade (2010-2019), bonds and commodities significantly outperformed stocks; only the energy, consumer staples and utility sectors recorded positive equity returns. The best performers: small cap stocks, consumer discretionary, financials, industrials, tech, staples and pharma. The worst performers: cash, commodities, value stocks, energy, telecoms, utilities and staples.

Currency returns since end of 1924 versus USD, log scale. Only three have out performed the US Dollar with 25 out of 55 falling more than -99%. CHF is the winner.

By far the most powerful predictor of long-term equity performance is the starting P/E or CAPE ratio. Source: Deutsche

History says that real returns are very bad in periods of either inflation or conflict. The 1970s were a period when it was very difficult to generate meaningful positive returns. And the decades of both world wars (1910s and 1940s) were weak when it came to asset returns.

Nominal returns for US assets over different time horizons

Real returns for US assets over different time horizons

Developed market nominal and real equity and bond returns (annualised)

Understanding the total cost of ETF ownership:

Bear markets and crashes:

Every bubble features a tendency to replace analysis with imagination.

The history of drawdowns: The historical evidence shows that equity drawdowns extending beyond 25 years that didn't see a recovery during this period are extremely rare in real terms, though the magnitude of losses within those exceptional cases can be severe.

At present, Greece and Kenya are the only markets experiencing such drawdowns exceeding 25 years. Both still have a long path to recovery. By contrast, Japan’s prolonged equity slump - a 33-year period of negative real returns - finally ended in 2022, marking the close of one of the longest continuous real equity drawdowns on record.

Material for meditation:

Bubbles are not neat linear processes. They typically inflate in several waves interspersed by dramatic falls. Looking at the dot-com bubble, the Nasdaq technology index surged and fell back by 10 percent or more seven times in the five years before it peaked on March 10, 2000.

It also carried on shooting into the stratosphere well after talk of a bubble became commonplace, doubling in the year to October 1999, then almost doubling again over the following five months until it turned.

The decline of the Nasdaq from its peak was also far from linear or immediate. The index fell by more than a third in 10 weeks, then recovered two thirds of its losses before finally declining in a saw-tooth pattern to a 78 percent peak-to-trough loss in October 2002.

Typical pattern of bubbles:

Weighting of Top 2 Holding in S&P 500 from 1980 to 2025:

During almost every recession in the US, equities (red diamonds) bottomed before all the other indicators that investors tend to follow. The indicator that is most closely associated with a bottom in equity markets: the ISM manufacturing survey. The big exception: the 2001/2002 tech collapse, when equities bottomed last. Bottom line: expect a lot of the economic and market news to still be very negative when buying financial assets at their lowest prices.

- JPM

Don’t get too excited about stocks and rate cuts. Based on history, U.S. stocks tend to decline significantly when the Federal Reserve transitions from a rate hike cycle to a rate cut cycle. Since 1970, there have been 9 instances when the Fed substantially lowered rates. The average maximum drawdown in stocks from the beginning of each rate-cutting period to the market bottom was 27.25%. In the last three episodes, the downturns exceeded the average level:

The weight of the biggest stock in the S&P 500 since the data began in 1981:

Deutsche Bank has analysed average inflation rates across 152 countries since 1971 and found that no economy—developed or otherwise—has successfully maintained a 2% inflation rate over the long term. The closest was Switzerland, with an average of 2.2%, followed by Germany and Japan.

The chart supports the case for assets with limited supply, such as cryptocurrencies, gold, and land. It also helps explain why the Japanese yen and Swiss franc are viewed as reliable safe-haven currencies:

The wealthiest 1% owns about half the US stock market:

The level of the S&P 500 that we associate with varying levels of the equity risk premium:

Details:

Laissez-faire economics, tax cuts and deregulation have historically driven rapid asset price inflation (e.g., Coolidge, Reagan presidencies;), as have technological booms (e.g., automobiles, radios in the 1920s, internet in the 1990s). 2025 presents the rare case of having a collision of both, as the Trump administration’s policy shift meets the AI revolution. Such a combination is one which we may not have seen since the Roaring ‘20s and amplifies right tail risks going into 2025, perhaps more so than many expect.

Taking profits during a significant rally is not just about securing your gains; it’s a strategic move to consolidate your wealth and avoid significant losses in case of a market reversal:

The size of our positions matter just as much as the positions themselves:

Nervous about investing when stocks hit all-time highs? Surprisingly, it could be a smart time to buy! (Mike Zaccardi)

Don’t rely on pensions from the state or any fund:

Don’t argue with fools:

1000 Years of Technological Disruption:

Stock market crash manual

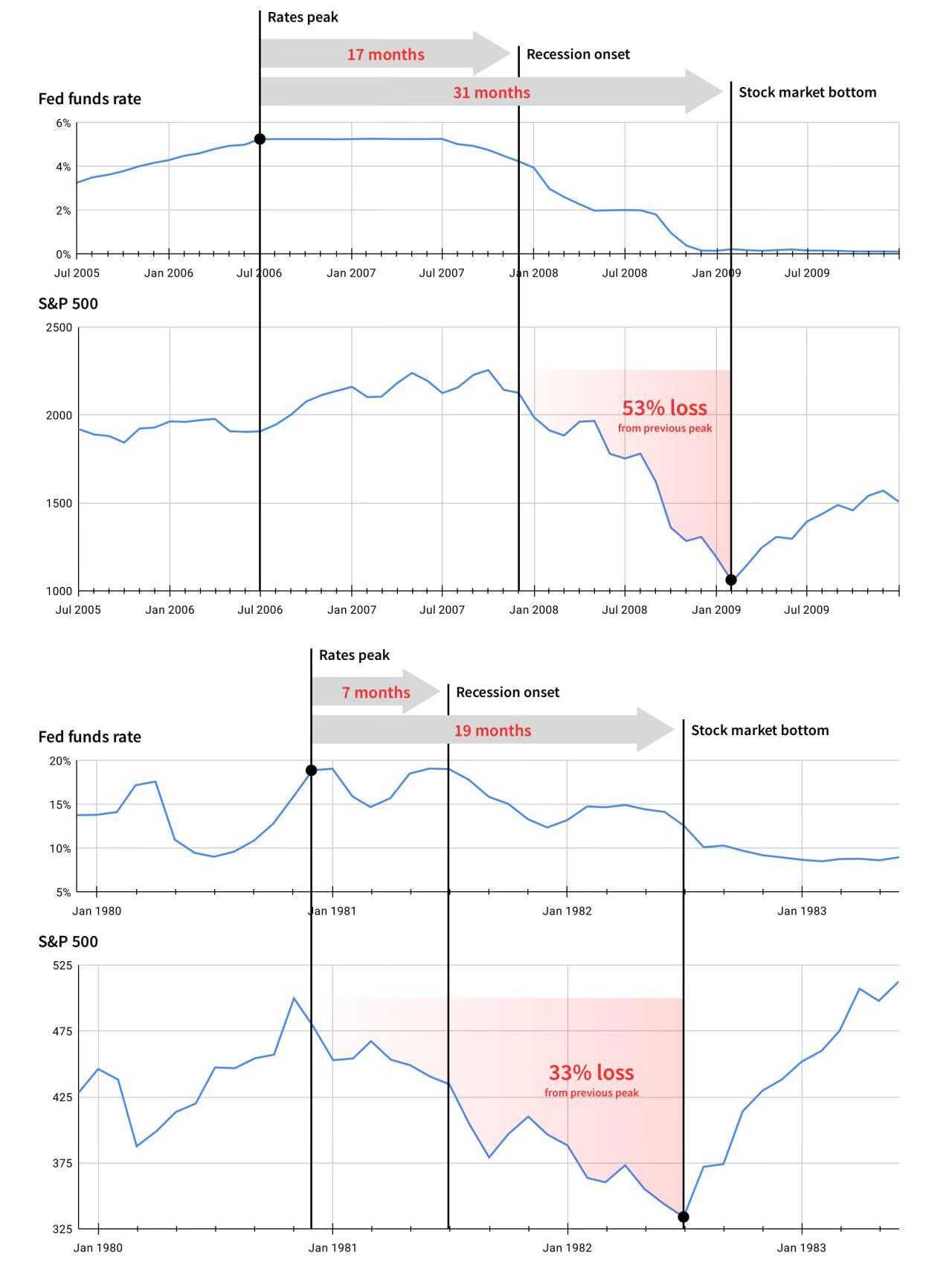

The Value of Patience in Bear Markets

Investors often worry about purchasing assets only to see their value plummet. The key factors to consider are the depth of the drawdown and the time required for recovery. This analysis examines the four major bear markets since 1900, focusing on their drawdown and recovery periods, as illustrated in Figure 36.

Wall Street Crash (1929–1945): US stocks reached their lowest point in July 1932, with recovery taking until February 1945 — a total of 15.5 years.

1973–1974 Bear Market: From January 1973 to October 1974, equities experienced a significant decline. In real terms, the market remained underwater for over 10 years.

Tech Bubble Burst (2000–2007): Following the peak in March 2000, US equity prices collapsed, with the full drawdown and recovery period lasting 7.5 years until July 2007.

Global Financial Crisis (2008–2012): The market hit its lowest point in February 2009, with recovery achieved in approximately 4 years.

Since 1920s, of the previous 59 corrections, only 17 became bear markets:

Reasons To Sell:

Patience has been valuable: Investors are often concerned about buying assets and then experiencing a dramatic fall in their value. The crucial issues are the depth of the drawdown and the time to recovery.

After the Wall Street Crash, US stocks fell to a trough in July 1932, and recovery eventually took until February 1945 - fifteen and a half years. The next large drawdown was from January 1973 until October 1974: in real terms, equities were underwater for over ten years. After the tech bubble burst in March 2000, US equity prices again collapsed and the full drawdown and recovery period lasted seven and a half years until July 2007. The subsequent Global Financial Crisis saw the market reach its nadir in February 2009. The market took four years to recover. (UBS)

Stop Worrying about Bear Markets:

US Market Downturns, Recoveries, and Expansions

How sharp bear market rallies can be:

"Missing just the 50 best trading days since the global financial crisis reduces the S&P 500's annualized returns from approximately 17% to around 3%, similar to bonds."

Again, let’s tell the full story here:

Effective diversification is the key:

Bear Market Playbook:

Magnitude and Duration of Drawdown

Magnitude of non-recessionary bears is a shallower -22% compared to the median -35% drawdown felt when bear markets coincide with recessions.

Duration of non-recessionary bears averaged only three months compared to 18 months for recessionary.

Monetary and Fiscal Policy Trends

All the recessionary bear markets occurred with an inverted yield curve.

In the only yield curve inversion where a recession was avoided, the deficit to GDP ratio increased by 3% during the period of fed tightening and curve inversion. This has also been true so far in current yield curve inversion period.

Investment Style Differentiation

Low Volatility and Dividend styles were the most resilient in drawdowns regardless of whether recessionary conditions were present.

Recovery performance in non-recessionary periods favored Quality and Growth compared to Value and Small Caps after recessionary bear markets.

Recessionary vs. Non-Recessionary

There are key differences in recessionary and non-recessionary bear markets.

The median drawdown for recessionary bear markets was -35%, about 50% deeper than non-recessionary bears. Non-recessionary bear markets are usually caused by temporary fear that the economy is stalling or entering a recession. And as positive data emerges, the fear — and drawdown — subside. The additional 10% to 20% drawdown seems to coincide with evidence of recession finally surfacing in the data, additionally supported by an extra year of duration as it digests the negative data (not sentiment). Interestingly, there was only one time in history that we have experienced back-to-back, non-recessionary bear markets, and that was during the fiscally supportive 1960s.

Bear Markets Tend to Run Deeper When Valuations Are High

US equity real returns (%), 1900–2024:

Investment Styles & Bear Markets:

United States is projected to reach a Global Market Cap of $116 Trillion by 2075, more than India, Japan, UK, France, and Germany combined! And about 60% higher than China!

Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves. (Peter Lynch)

Most Popular Stocks Among U.S. Retail Investors:

"Europe has industries from last century and does not participate in the current tech revolution":

A Reminder of the Math Behind Losses:

A stock that drops 70% needs to gain 233% just to break even. Challenging—but still within the realm of possibility.

But a 99% drop? That requires a 9,900% gain to recover. At that point, it’s not a comeback—it’s a miracle.

But there is always some exceptions:

Strategies overview

The 10% Edge: How Small Bets Rewrite History and Redefine Tomorrow:

Midterm metters:

Anyone chasing this market higher here should understand where we are in the cycle. This is historically the weakest part of the presidential pattern, the phase where momentum usually starts to fade and the market often goes through its real reset. On average, that reset has been around 16%, which means the easy upside may already be behind us. Anyone treating this like a clean breakout phase instead of a potentially dangerous late-stage stretch is probably looking at the wrong part of the bigger picture. The risk here is not missing a few more percent up, but getting caught too early before the real correction does its work.

Anyone who understands the cycle also knows that the correction is usually not the end of the story, but the setup for the next one. In 19 out of 19 cases, the mid-term correction was followed by a two-year bull market, which is as close to a clean historical pattern as you get. That is why my own approach is not to buy blindly now and not to panic later, but to let weakness come and then build a position step by step. My structure would be 31% of tactical capital around minus 8%, 23% around minus 12%, 18% around minus 16%, 12% around minus 20%, 9% around minus 25% and the last 6% around minus 30%. I would also adapt to the type of selloff, moving faster if panic creates a sharp flush and slower if macro conditions keep deteriorating. The message is simple: anyone chasing the top is late, but anyone prepared for the reset may get the best entry of the cycle.

Supporting data from Mark Hulbert: the "sell in May" phenomenon is almost entirely a result of Presidential Cycle Year 2 seasonality. In Midterm years (like 2026) there is a 9.3% discrepancy between the two periods versus just a 1.3% difference in the other three years.

Terry Marsh, an emeritus finance professor at the University of California, Berkeley and Kam Fong Chan, a professor of finance at the University of Western Australia posit this midterm pattern is a result of an elevated level of uncertainty before the midterms and the resolution of that uncertainty after the midterms.

Global M2 is the chart that matters.

The rally is being driven less by falling yields and more by liquidity, positioning and balance-sheet impulse. Bitcoin usually sniffs this out earlier than equities. When global liquidity improves, BTC often moves first, high-beta equities follow and the S&P 500 eventually starts pricing the same impulse more slowly and institutionally, through the credit channel, earnings confidence and risk appetite.

The key signal now is credit. If spreads stay contained while global M2 keeps expanding, the market can keep climbing even with yields elevated. That is the uncomfortable part for bears: headlines may scream tightening, but the asset-price channel can still behave like liquidity is improving.

So the simple rule is:

Rising global M2 = more money in the system.

High yields = money is expensive.

Wide credit spreads = people are scared.

High yields with low spreads = expensive money, but no panic.

High yields with rising spreads = expensive money plus panic.

That last one is much worse for stocks.

Charts to watch:

1. M2 vs S&P 500

https://streetstats.finance/liquidity/money

2. Bond Yield Credit Spreads (last 90y)

https://www.longtermtrends.com/bond-yield-credit-spreads/

3. ICE BofA US High Yield Index (last 3y)

https://fred.stlouisfed.org/series/BAMLH0A0HYM2

Gold matters:

Follow the money - the environment catalysed by QE created optimal conditions for #gold to perform well, tracking the rapid expansion in the US money supply:

Since 1971, with few exceptions, gold has significantly outperformed all major currencies and commodities as a means of exchange. A key factor behind this robust performance is that gold mine production has grown slowly – increasing by approx. 1.7% per year over the past 20 years:

Visually: How much gold is there in the world?

If we took all the gold ever mined and melted it into a big cube, it would be this size (edge length 21 meters). Throughout human history, 216,000 tons have been mined—a small size for such a valuable metal with a market cap already over $12 trillion.

"Since 2005 the amount of gold discovered declined by 50% every 5 years. We are running out of new gold."(Willem Middelkoop)

US market vs World, “Rome” is collapsing

“America Is Collapsing Like Rome” - what happens next?

Why U.S. Equities Will Outperform European Markets in the Coming Years:

A Brief Guide to Speculative Trading Ahead of a Nuclear Apocalypse:

Market Pressure and Investment Illusions:

US Fed Funds target rate, %

Interest rates since 3000BC:

War is expensive & inflationary:

Federal Reserve balance sheet % of GDP since 1914:

US government expenditures % GDP since 1791:

Rates, returns & valuation in 21st vs 20th century:

Annual returns in 2010s…10% in deflation assets (bonds, tech…), 6% in inflation assets (cash, commodities, value…); thus far 2020s…5% deflation vs 4% inflation. We sell US dollar & deflation assets such as IG bonds & monopolistic tech/growth stocks into coming recession, we buy inflation assets such as commodities, real estate, value cyclicals as recession begins:

Banks vs S&P 500 (price relative):

Old Schooll Value:

General Thoughts Serving as a Conclusion:

Stand in solidarity:

Breaking the German law: Édith Piaf and the Prisoners, Germany, 1944:

The real luxuries in life: no mention of job or something similar. Not even close. It’s about a mindset that normalizes exploitation as necessary or even noble. Romanticizing “stability” of a “job”while ignoring what’s being sacrificed to get it is exactly how modern chains stay invisible.

Reflect:

and finally:

- “We would own Wall Street.” - “But what do we do when we own Wall Street?” - “We burn it to the ground, and bring all the lemon farmers, roast marshmallows by the fire.” ("The Hummingbird Project")

Description of Democracy from Edward Bernays:

The conscious and intelligent manipulation of the organized habits and opinions of the masses is an important element in democratic society. Those who manipulate this unseen mechanism of society constitute an invisible government which is the true ruling power of our country. We are governed, our minds are molded, our tastes formed, and our ideas suggested, largely by men we have never heard of…. It is they who pull the wires that control the public mind.

“There have been sixteen cases over the last 500 years in which a major nation’s rise disrupted the dominant state. Twelve of these rivalries ended in war and four did not according to political scientist Graham Allison, author of “Destined for War: Can America and China Escape Thucydides’ Trap?” In 2018, I wondered how much the US-China relationship might be affected by economic linkages which could mitigate the risks of conflict. I was encouraged by my findings at the time. I added the outstanding stock of bilateral foreign direct investment, the amount of bilateral annual trade and the stock of government bonds owned by the other country’s Central Bank. As shown on the left, the China/US economic linkages were much greater than those between the 20th and 21st century parallels I could find.

My optimism might have been misplaced at the time, and a lot has changed since then: stagnating Chinese holdings of US government bonds”, a decline in the stock of US-China foreign direct investment from peak levels and the onset of a trade war. Our latest estimate for US-China linkages is now -4% of combined GDP, down from 7.3% in 2014.”

Michael Cembalest, JPM

In my opinion we should trust no one, but often we are forced to trust strangers because it looks like we have no other choice. What I trust is the process, because truth emerges not from fleeting promises, but from the dynamic verification of actions, outcomes, and adaptations.

Die Lüge wird zur Komfortzone. Der Irrtum zur Identität. „Wir glauben, was unsere Gruppe glaubt“. Wer aus der Herde ausschert, verliert Zugehörigkeit. Menschen sehen nicht, was ist – sondern was sie verkraften können. Wahrheit wird zur Zumutung. Die größte Illusion dabei: Man fühlt sich frei. Man geht zur Arbeit, postet seine Meinung, wählt alle vier Jahre – und merkt nicht, dass der Spielraum längst enger geworden ist.

“It is better to be roughly right than precisely wrong.” - Alan Greenspan

Die Lüge wird zur Komfortzone. Der Irrtum zur Identität. „Wir glauben, was unsere Gruppe glaubt“. Wer aus der Herde ausschert, verliert Zugehörigkeit. Menschen sehen nicht, was ist – sondern was sie verkraften können. Wahrheit wird zur Zumutung. Die größte Illusion dabei: Man fühlt sich frei. Man geht zur Arbeit, postet seine Meinung, wählt alle vier Jahre – und merkt nicht, dass der Spielraum längst enger geworden ist.

Wir brauchen keine Helden, die im Krieg sterben. Wir brauchen Helden, die Kriege und Blutvergießen verhindern:

Zuerst kommt ein Wohlstand wie noch nie.

Dann folgt ein Glaubensabfall wie nie zuvor.

Darauf eine nie dagewesene

Sittenverderbniss.

Alsdann kommt eine grosse Zahl

Fremder ins Land.

Es herrscht eine hohe Inflation.

Das Geld verliert mehr und mehr an Wert.

Bald darauf folgt die Revolution.

Alois Irimaier 1894-1959

Der fatale Fehler des 19. Jh. war die Reichsgründung 1871 – aus Kleinstaaten wurde ein imperialer Machtblock. Im 20. Jh. ließ man Deutschland nach WWI unangetastet – das Ergebnis war WWII. 1990 dann der dritte Fehler: die Wiedervereinigung um jeden Preis.

Im 21. Jh. eskaliert dieses Deutschland den Ukrainekrieg, liefert Waffen, hetzt gegen Verhandlungen und will Europa militärisch führen.

In Ostdeutschland marschiert gleichzeitig eine AfD mit Mehrheit auf, die demokratische Grundordnung verachtet. Die Spaltung ist längst da.

Wer meint, man könne dieses Land noch integrieren, verkennt die Geschichte. Die Frage ist nicht, ob Deutschland wieder zerfällt – sondern ob es diesmal rechtzeitig und friedlich geschieht.

Wer klug ist, zieht die Grenze mit Stift – bevor es wieder andere tun und es brennt.

The top 10% of Americans held 93% of all stocks, the highest level ever recorded. Meanwhile, the bottom 50% of Americans held just 1% of all stocks.

What if we used 100% of the brain?

YOU START MOVING AWAY FROM GERMANY

“Thinking is difficult, that’s why most people judge.” ~ Carl Jung

“The stock market has predicted nine of the last five recessions.” - Paul Samuelson, economist, 1966

They create the problem, then sell you the solution -for a profit, of course.

Hat schon jemand versucht, Asyl mit dem deutschen Pass in Neuseeland zu beantragen? Frag‘ für einen Freund.

“The slave dreams not of freedom, but of his own slaves.” - Cicero

“I made my money by selling too soon.”

— Bernard Baruch

“If you don’t know who the fool is at the table, it’s you.”

- Warren Buffett

“Those who fight Nazis, cannot rely on the state” - Esther Bejarano

My forecast for the Swiss franc: it will most likely increasingly correlate with the price of gold.

»Wem es an Sex fehlt, der spricht über Sex. Wer hungrig ist, redet über Essen. Wer kein Geld hat, redet über Geld. Deshalb reden Politiker und Banker über Moral.«

Sigmund Freud

Fritz Bauer about West Germany: „Always when I leave my office, I enter enemy territory.“

A prosecutor as a Nazi hunter: Fritz Bauer was born on July 16, 1903. As the Hessian Attorney General since the 1950s, Bauer made significant contributions to the investigation and prosecution of Nazi regime crimes. In 1963, at his initiative, the Auschwitz trials were held against those responsible for the Nazis’ largest extermination camp. These trials provided a crucial impetus for confronting the Holocaust in the old Federal Republic.

However, Bauer repeatedly faced substantial resistance from West German law enforcement agencies, where many former Nazi jurists held high positions.

This is also why he disclosed Adolf Eichmann’s whereabouts in Argentina to the Israeli Mossad rather than the German authorities, whom he did not trust.

„Wer die Wahrheit sagt, braucht ein schnelles Pferd“

“The state is the coldest of all cold monsters:

Everything about it is false;

it bites with stolen teeth.

It even speaks with the mouth of the people.

It says: ‘I, the state, am the people.’

That is a lie!”

- Part I, “The New Idol” Friedrich Nietzsche

The biggest drive for financial independence is the freedom to avoid working with and living around people you don’t like.

“This entire market has been based on people not understanding that, imagining that scaling was going to solve all of this, because they don’t really understand the problem. I mean, it’s almost tragic.”

“Time is not money”

Time is not a resource that can be earned, saved, or spent like money. It’s an intangible and finite asset that continuously flows forward, indifferent to our attempts to control or manipulate it.

In essence, time is the fabric of life itself. It is the essence that weaves our experiences, relationships, personal growth, and impact on the world. While money has its place in our society, it is time that holds the most accurate and most profound value.

Unlike money, which can be earned, lost, or even regained, time, once used is irretrievable. Every second that slips away is a moment of our lives that can never be reclaimed. While money can provide comfort, security, and access to material possessions, it cannot grant us more time.

Time, on the other hand, offers us the opportunity to create meaningful connections, pursue our curiosities, learn, grow, and experience the world meaningfully. It is the currency we invest in ourselves and the moments that truly shape our lives.

Time is free, but it’s priceless. You can’t own it, but you can use it. You can’t keep it, but you can spend it. Once you’ve lost it you can never get it back.

Time, unlike money, is an inherently democratic entity. It’s an equally distributed asset, regardless of our financial status or societal standing. Whether wealthy or poor, successful or struggling, you have the same 24 hours in a day to make a difference in your life. This egalitarian nature of time highlights its profound value as a universal currency that transcends economic disparities.

Given how precious time is, we should put it first. But many of us focus on our careers, constantly giving up more of our time in exchange for more money or productivity.

The experiences we have, the relationships we forge, and the memories we create are not determined by our financial wealth but by the choices we make with the time we are given. Money may provide access to luxuries, but it is time that allows us to appreciate and cherish the richness of our existence.

We must not allow the clock and the calendar to blind us to the fact that each moment of life is a miracle and mystery.

Sources and inspiration X channels:

Stocks / Finance / Markets

😂 Memes / Culture

Useful websites:

https://whalewisdom.com/filer/zurich-insurance-group-ltdfi

https://whalewisdom.com/filer/meag-munich-ergo-kapitalanlagegesellschaft-mbh

https://www.nbim.no/en/investments/all-investments/#/

https://finviz.com/

https://www.holdingschannel.com/

https://www.zinsen-berechnen.de/zinsrechner.php

https://www.zinsen-berechnen.de/zinseszinstabelle.php

https://www.portfoliovisualizer.com/backtest-portfolio

https://www.savvyinvestor.net/articles-and-white-papers

https://www.fastbull.com/

https://www.edwardconard.com/macro-roundup/topic/gdp/financial-markets/

https://gqg.com/insights/

https://www.dbresearch.com/PROD/RI-PROD/Research_Institute/HOME.alias

http://www.freeintertv.com/view/id-370/USA-News-2-1?chname=bloomberg&findch=1

https://wtfhappenedin1971.com

https://www.allianz.com/en/economic_research/insights/publications.html

https://transferpricingnews.com/category/latest/

https://www.pwc.com/gx/en/services/tax/publications/international-tax-news.html

https://business.bofa.com/en-us/content/market-strategies-insights/weekly-market-recap-report.html

https://business.bofa.com/en-us/content/market-strategies-insights.html

https://am.gs.com/de-de/institutions/insights

https://www.jpmorgan.com/insights/research/reports

Telegram channels:

Stocks:

@bloomberg_shelf

@truefinance

@geonrgru

@energytodaygroup

@proeconomics

@needleraw

@east_shift

@crimsondigest

@viktor_pershikov

@moi_misli_vslukh

@vestifinance_ru

@malekdudakov

@angrybonds

@markettwits

@grechne

@khtrader

@wublockchainenglish

@ifinvest

@PiQsReutersHeadlineFeed

@roflpuls

@tomcapital

@delyagin

@economylive

@primenumbers2021

@politpe

@cryptopizza_news

@thefinansist

@telran_invest

@the_block_crypto

@DeCenter

@cryptotweet280

@otdyshiprocrypto

@investmemes

@PirogovLive

@eumoney

@t_analytics_official

@sgcapital

@MarketHeart

@energopolee

@trading_broker

@Cringedaily

@truecon

@sttonks

@inflation_shock

@warwisdom

@alexbobrowski

@ira_Akhmadullina

@naebrosh

@MarketDumki

@true_flipper

@ExencialResearch

@econbox

@BeglaryanCapital

@isurion

@ikapralov

News & Tech:

@ru_tech_talk

@tzdjournal

@lsbcurator

@aboutplane

@TrendWatching24

@citizenshipmaster

@F_S_C_P

@glavmedia

@kozakrichala

@r_mapporn

@indeec_1937

@antidigital

@yo_history

@india_tv2020

@Black_History

@Fourier_series

@it_secur

@rationalnumbers

@kosmo_off

@medicalksu

@rezident_ua

@sustaincoll

@demographic_autism

@pustota1058

Media:

@muscatmovies

@itsallinenglish

@muscatenglish

@muscatenglish

@trunkietrunk

@kappienglish

@zvukidlyasosedei

@everythingenglishua

@Modnayazheleza